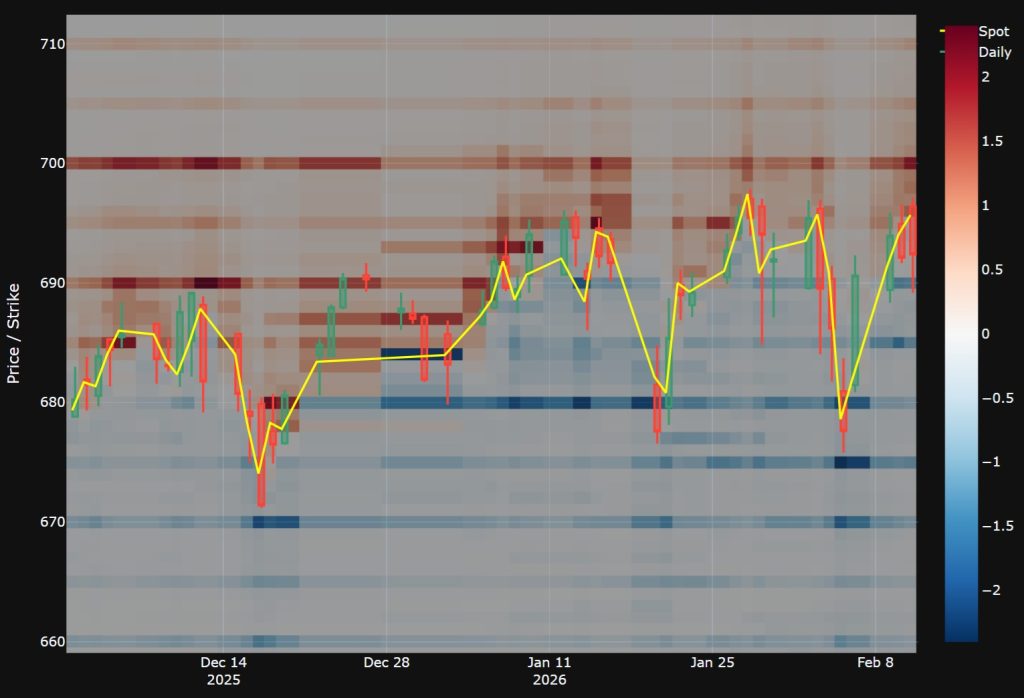

OPENINTEREST conducts research on hedging flows in the U.S. equity options market.

Our primary focus is the impact of dealer gamma positioning on intraday price dynamics.

We analyze how aggregate options positioning translates into mechanical hedging activity and how this flow interacts with liquidity, volatility, and short‑term market structure.

OPENINTEREST develops analytical software focused on dealer positioning and hedging mechanics in the U.S. options market.

Our work integrates quantitative modeling with real‑time market execution. The research is directly applied to trading strategies in index, stock and ETF options.

Core analytical components include:

Gamma Exposure (GEX) modeling

Vanna Exposure (VEX)

Charm Exposure (CEX)

Options Time & Sales analytics for intraday and medium-term deals

Dealer hedging pressure and spot impact modeling